Coalition Agreement Between CDU/CSU And SPD Fundamentally Sets The Right Priorities, Says WDK

- By TT News

- April 11, 2025

The German Rubber Industry Association (wdk) has said in its latest statement that the coalition agreement between the CDU/CSU and the SPD essentially establishes the correct goals from the standpoint of the German rubber industry.

The promises to technical openness in the automobile sector, to cutting bureaucracy and to a risk-based approach in chemicals policy are undoubtedly welcome, according to Michael Klein, President, wdk. He said that the Supply Chain Due Diligence Act's announced repeal is a significant step towards reducing the burden on businesses and will satisfy the rubber industry's requests during the election campaign.

Praising the announced support for the circular economy, he said, "Waste tyre recycling, in particular, is a prime example of the diverse and successful possibilities of using recycled materials and tyre retreading. The coalition partners would have liked to have highlighted rubber products more clearly here. The promises to reduce bureaucracy are also in line with the demands of the business community. This is especially true for bureaucracy practice checks, which were proposed by the wdk."

But before any real action is done, he also warned that nothing is as it seems because prior government coalitions have also pledged to lessen the various reporting obligations. The executive lamented that the coalition agreement did not specifically target energy-intensive, industrial SMEs and made no mention of market monitoring, although applauding the announced relief for industry from high energy costs.

"Now it's important to breathe life into the letter of the coalition agreement and implement the agreed measures promptly and in close dialogue with the business community. The German rubber industry is happy to provide its expertise for this purpose and will continue to closely and critically monitor the implementation of the agreements,” concluded the wdk President.

JK Tyre Raises Product Prices Amid Raw Material Surge

- By Sharad Matade

- August 11, 2026

JK Tyre & Industries has increased product prices and signalled further hikes as it seeks to offset rising raw material costs, even as demand remains resilient across segments.

The company said raw material prices rose about 20 percent quarter on quarter, with a further 8–10 percent increase expected in the following quarter. The increase has put pressure on margins, given that about 70 percent of tyre industry inputs are petro-based.

In response, JK Tyre raised product prices by 10–11 percent until August and plans an additional increase of 5–6 percent in the coming months to mitigate cost pressures.

The pricing action comes despite steady demand conditions. The company reported a 25 percent year-on-year increase in domestic volumes in the June quarter, supported by growth across both replacement and original equipment manufacturer segments.

Management indicated that demand remained stable across commercial vehicles, passenger vehicles and two- and three-wheelers, with no significant production cuts from OEM customers.

The company also said it continues to focus on premiumisation, with higher-margin products such as 16-inch and above passenger car tyres increasing their share in the sales mix.

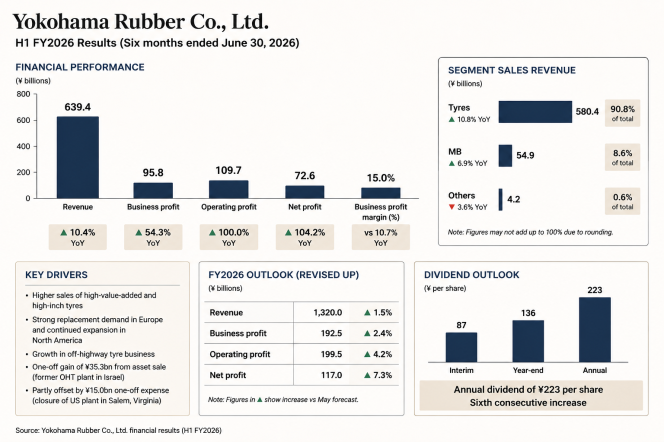

Yokohama Rubber H1 Profit Soars More than Double And Raises Full-Year Outlook

- By Sharad Matade

- August 11, 2026

Yokohama Rubber reported record earnings for the first half of fiscal 2026, with profits more than doubling and margins reaching a historic high.

The Japanese tyre maker said sales revenue rose 10.4 percent year on year to ¥639.4 billion in the six months to June, while business profit increased 54.3 percent to ¥95.8 billion. Operating profit doubled to ¥109.7 billion, and profit attributable to owners of the parent rose 104.2 percent to ¥72.6 billion.

Business profit margin improved to 15.0 percent, compared with 10.7 percent a year earlier, marking a record level for the company.

Yokohama Rubber said the results reflected strong performance across its businesses, delivering record first-half highs in all key earnings categories.

Segment data showed that tyre sales revenue rose 10.8 percent year on year to ¥580.4 billion, accounting for 90.8 percent of total revenue, while the MB (Multiple Businesses) segment recorded revenue of ¥54.9, up 6.9 percent and contributing 8.6 percent of the total. Other businesses declined 3.6 percent to ¥4.2 billion.

Business profit growth was led by the tyre segment, where profit increased 57.3 percent to ¥89 billion. The MB segment posted profit of ¥6.3 billion, up 22.5 percent, while other businesses reported profit of ¥0.5 billion.

The company said tyre segment growth was supported by higher sales of high-value-added and high-inch tyres, as well as increased volumes in the off-highway tyre business. Replacement tyre demand strengthened across regions, with strong sales in Europe and continued expansion in North America.

Operating profit was also supported by a ¥35.3 billion gain on the sale of assets at a former off-highway tyre plant in Israel, partly offset by a one-off expense of ¥15.0 billion related to the closure of a US tyre plant in Salem, Virginia.

The company also revised upwards its full-year forecast for fiscal 2026. It now expects sales revenue of ¥1,320 billion, business profit of ¥192.5 billion, operating profit of ¥199.5 billion and profit attributable to owners of the parent of ¥117 billion.

JK Tyre Reports Steady Quarterly Revenue As Margins Face Pressure

- By TT News

- August 10, 2026

JK Tyre & Industries reported broadly steady revenue for the first quarter of the financial year, with profitability constrained by higher input costs.

The company posted consolidated revenue of INR 39.56 billion for the quarter ended 30th June, 2026, while earnings before interest, tax, depreciation and amortisation (EBITDA) stood at INR 2.68 billion, implying a margin of 6.8 percent. Profit before tax was INR 0.54 billion and profit after tax came in at INR 0.43 billion.

According to the company’s financial statement, revenue from operations was INR 39.46 billion, compared with INR 38.69 billion in the corresponding period a year earlier.

Operating profit declined to INR 2.68 billion from INR 4.24 billionn a year earlier, reflecting pressure on margins.

Dr Raghupati Singhania, Chairman and Managing Director, said: “JK Tyre continued its steady performance in Q1FY27 with a consolidated turnover of INR 3.56 billion, supported by strong demand momentum across segments. The performance is driven by sharp focus on customer centricity, product excellence and disciplined execution across markets. During the quarter domestic volumes grew by 25 percent on year-on-year basis, across both replacement (12%) and OE markets (42%), with increasing contribution from higher-value added products. The continuing west Asis crisis led to a sharp increase in raw material prices which impacted our gross and operating margins. As is known approximately 70 percent of the tyre industry raw materials are petro based, hence, it is highly vulnerable to oil price movement”.

He added: “With a sharper focus on operating leverage, cost reductions, and increasing share of premium products, JK Tyre remains confident to improve performance in FY27 with double-digit revenue growth, aiming to create enduring value for all stakeholders with an increased profitability through strategic expansions”.

Dunlop And Beta Motorcycles Strengthen OE Ties With New Geomax Tyre Lineup

- By TT News

- August 08, 2026

Dunlop Motorcycle Europe has expanded its original equipment partnership with Beta Motorcycles, securing a deal to supply advanced Geomax tyres across the Italian brand’s trial and motocross lineups. The enhanced collaboration introduces new standard fitments for both competition disciplines.

For trial applications, the Geomax TL01 replaces the previous D803GP on Beta’s Evo and Sincro models. Engineered with a high-adhesion compound and a specialised block layout for angled terrain, the ultra-sticky tyre has already proven popular among Beta racers and now becomes factory-standard equipment.

In the motocross sector, Beta has adopted the Geomax MX34 for its entire RX range, covering both two-stroke and four-stroke 250 cc and 350 cc variants, as well as the 450 cc model. Designed primarily for intermediate ground, the versatile MX34 performs effectively across diverse surfaces, from soft mud to compacted dirt.

Donato Miglio, Race Team Manager Trial, Beta Motorcycles, said, "Geomax TL01 represents a significant step forward in performance, which is why we decided to adopt it as our original equipment trial tyre. Many of our riders already use it in competition, where it has proven its exceptional grip, stability and handling.”

Fabrizio Dini, Race Team Manager Motocross and Enduro, Beta Motorcycles, said, “In motocross, the latest generation of Dunlop MX tyres features significant performance improvements. Geomax MX34 provides excellent grip, particularly on dry surfaces, giving riders a reassuring feeling of safety and constant control. Both tyres suit our bikes perfectly.”

Miguel Morais, Original Equipment Manager, Dunlop Motorcycle Europe, said, “We are proud to deepen our partnership with Beta through the introduction of Geomax TL01 and MX34 across its latest trial and motocross models. Fitments like these are a strong endorsement of the capabilities of tyres throughout our range, and we’re excited that more and more riders will experience increased confidence and performance that helps them get the most out of their Beta motorcycles from their first ride.”

Comments (0)

ADD COMMENT