Retreading’s Stubborn Struggle

- By Gaurav Nandi

- August 29, 2025

Despite decades of presence and proven sustainability benefits, the global truck tyre retreading industry remains mired in perception problems and systemic inertia. As raw material costs rise and environmental pressures mount, retreading should be a no-brainer. Yet, it continues to be sidelined by outdated mindsets, customer ignorance and a lack of cohesive industry messaging. Tirecore CEO Garry Drisdelle, in a candid interview with Tyre Trends, paints a picture of a sector at risk – not because it lacks value, but because it has failed to communicate it. The stakes, he warns, are too high for complacency.

Despite decades of existence, the retreading industry still wrestles with fundamental challenges across the world – not least the stubborn perception among customers and stakeholders about the true value of retreaded truck tyres. Tirecore Chief Executive Officer Garry Drisdelle pulls no punches in diagnosing the sector’s issues and outlining the uphill battle ahead.

Speaking to Tyre Trends, he said, “Tirecore is primarily a supplier of quality truck tyre casings to the retread industry. But while retreading should logically form the cornerstone of sustainable tyre use, the industry remains far from mainstream acceptance.”

“Educating the customers really as to how much upcycling, how much can we save – it’s beyond the pennies or pounds you save on the initial purchase,” Drisdelle said. Yet, frustratingly, many customers remain fixated on upfront costs instead of the total lifecycle value of a tyre.

This fixation, he implies, represents a systemic failure within the industry. “The industry has to do a better job towards educating the consumers, which primarily are fleet owners, beyond the initial purchase,” said Drisdelle. The inability to shift consumer mindset threatens to leave retreading as a niche rather than a necessity.

Tirecore positions itself primarily as a global supplier of high-quality truck tyre casings to the retread industry, operating across markets that include the United States, Canada and India. Rather than manufacturing or retreading tyres directly, the company serves as a critical node in the circular economy of commercial tyres, ensuring that valuable casings find extended life through retreading.

“We are in the business of preserving 85 percent of the tyre components existing material’s value saving valuable resources,” said Drisdelle.

The company’s operational model is rooted in the principle of upcycling over replacement, focusing on longevity and material reuse rather than disposability. While Tirecore’s precise logistical affiliations remain unspecified, its strategic direction is clearly aimed at aligning with sustainability mandates and evolving global market demands.

DISPOSABLE TREATMENT

Drisdelle highlights a critical contradiction. Tyres are one of the most safety-critical components on the road, yet they are taken for granted at a staggering scale. “Picture a truck is rolling down the highway at 100km/h pulling 20,000 kilogrammes of freight, riding on just 6-8-10 rolling rubber contact points. Tyres are one of the most critical transportation components, yet we treat them like disposable goods. How taken for granted is that product?”

Even as raw material prices surge and truck tyre costs climb, the entrenched perception treats tyres as disposable consumables. “We need to reframe the conversation – a tyre should be seen as an asset and not a consumable,” Drisdelle emphasises.

This disconnect reveals deeper issues prevalent within the industry. Retreading has not been effectively communicated as a financial and environmental beneficial in the long tome. Moreover, legislative inconsistency and lack of incentives for the industry as a whole is a deterrent that needs to be addressed immediately.

Drisdelle insists that retreading should be the environmental rallying point for the sector. “We have 85 percent of the material in the original product that is quite capable of being reprocessed and upcycled many times,” he said.

Drisdelle insists that retreading should be the environmental rallying point for the sector. “We have 85 percent of the material in the original product that is quite capable of being reprocessed and upcycled many times,” he said.

He contrasts upcycling favourably with recycling, which he argues requires more energy and effort than the original production process, especially in plastics and other materials: “By the time you just recycle something, the energy to recycle it is more than the process.”

Yet these arguments come with an implicit critique that the industry has failed to effectively translate this environmental rationale into a compelling value proposition for customers and regulators alike.

LEGISLATIVE MOMENTUM

Drisdelle points to potential legislation requiring truck tyres to be recyclable or retreadable as a possible catalyst for change. “Picture if legislation comes out that you’re not allowed to sell truck tyres unless they’re recyclable from their ingredients unless they’re retreadable,” he noted.

However, he quickly tempers this with realism stating, “We can never get to zero. That’s a cool little marketing thing but it’s an impossibility in the world of physics and science.”

This admission highlights the gap between aspirational sustainability goals and practical realities, a gap that leaves retreading vulnerable to accusations of greenwashing or insufficient progress.

ADAPT OR STAGNATE

Looking to the future, Drisdelle’s plan is pragmatic but cautious. “Our future plans are to keep up with the market demand, to evolve as the market evolves. Pivot and prosper,” he said.

Such a measured approach reflects the uncertainty and fragmentation within the industry. The promise of retreading remains strong, but without decisive action on education, regulation and innovation, the sector risks losing ground to cheaper, new tyres or alternative technologies.

The recurring theme throughout Drisdelle’s commentary is education, or rather, the lack of it. “The education of the fleet owners is primary to everything. The education of the industry to build a better tyre is somewhat secondary,” he stated.

This stark admission speaks volumes. Despite retreading’s environmental and economic advantages, a fundamental communication failure continues to hobble the industry.

Drisdelle points out the irony stating, “Without a widespread cultural shift in perception, retreading will struggle to move beyond a cost-saving niche for price-sensitive fleets to a mainstream standard.”

Drisdelle’s blunt assessment of the retread industry reveals a sector caught between its potential and its persistent shortcomings. Tirecore’s role as a global supplier to retreaders is clear but the wider challenge remains.

Without significant progress on education and regulatory backing, the retread industry risks remaining on the margins, overshadowed by the convenience of new tyres and the pressures of market inertia.

Retreading’s promise is substantial. But, as Drisdelle’s comments underscore, fulfilling that promise demands a candid reckoning with the industry’s educational failures and a relentless push for change or face stagnation in a rapidly evolving tyre market. n

Retreading In The Age Of EPR: Latin America Between Circular Ambition And Strategic Blind Spots

- By Daniel Rojas Enos

- July 01, 2026

As Extended Producer Responsibility (EPR) frameworks expand globally, the tyre industry is undergoing a structural transformation. Collection systems are improving, traceability is increasing and investments in recycling technologies are accelerating. However, one critical tension remains insufficiently addressed: the speed of industry evolution is outpacing the agility of public policy. And within that gap, one key question emerges: where does retreading fit in this new circular economy architecture?

A STRUCTURAL PARADOX

Retreading represents one of the most efficient forms of resource optimisation in the tyre lifecycle. It extends product life, reduces raw material consumption and lowers emissions. Yet, in many regulatory frameworks, it is still treated ambiguously – often grouped with recycling rather than recognised as prevention or preparation for reuse. This distinction is not semantic. It is strategic. Because when policy fails to differentiate, markets fail to prioritise.

A FAST-MOVING INDUSTRY, A SLOW-MOVING FRAMEWORK

The tyre market is evolving in real time:

- Increasing penetration of low-cost imports.

- Growing variability in product quality.

- Accelerated turnover cycles.

Retreading, in this context, becomes more than a circular solution. It becomes a filter of industrial quality. Not all tyres are equally retreadable. And that difference defines their real contribution to circularity. Yet most EPR systems continue to operate with uniform economic signals, failing to distinguish between products that enable multiple lifecycles and those that exit the system after a single use.

SIGNALS FROM EUROPE

Recent developments in countries like Portugal – where eco-fees applied to retreaded tyres approach those of low-cost, non-differentiated new tyres – highlight a concerning trend. Similarly, in Spain, industry representatives continue to advocate for a clearer institutional recognition of retreading within EPR systems. These cases illustrate a broader issue: circular policies can unintentionally undermine higher-value circular strategies.

THE MISSING LINK: PERFORMANCE-BASED POLICY

What is missing is not regulation. It is regulatory precision. EPR systems have successfully organised waste flows. But they have not yet evolved to reward performance within the lifecycle. This is where eco-modulation becomes critical.

ECO-MODULATION AS A STRATEGIC LEVER

Eco-modulation should not be a marginal adjustment. It should be a core industrial policy tool. Properly designed, it can:

- Differentiate tyres based on real circular

- performance.

- Incentivise durability and retreadability.

- Penalise short-lifecycle, non-recoverable products.

- Align market behaviour with system objectives.

- To operationalise this, we need new metrics.

FROM COMPLIANCE TO PERFORMANCE: A PROPOSED FRAMEWORK

The next step for EPR systems is to move towards performance-based differentiation. This could be implemented through instruments such as:

- Retreadability Index (RI)

- Performance Score (CPS)

These would measure:

- Number of effective retreading cycles per tyre.

- Structural durability and casing quality.

- Real contribution to lifecycle extension.

Under such a system:

- Tyres with higher retreadability would receive lower eco-fees.

- Products that systematically fail to re-enter the cycle

- would face higher costs.

- This is not just a technical refinement. It is a shift from:

- Generic compliance.

- To intelligent market shaping.

THE LATIN AMERICAN PERSPECTIVE

In Latin America, the stakes are even higher.

The region faces:

- Structural dependence on imported tyres.

- Strong presence of low-cost, low-durability products.

- Emerging EPR frameworks (Chile, Costa Rica, Peru, Ecuador)

Chile, for example, through its EPR law (Ley REP), has made significant progress in structuring collection and recovery targets. However, like many systems, it still faces the challenge of fully integrating reuse strategies into its economic logic. Under these conditions, retreading is not just an environmental solution. It is a strategic industrial capability.

BEYOND WASTE MANAGEMENT

Latin America has a unique opportunity to design EPR systems not only to manage waste

but to govern resources and shape markets.

This means:

- Incentivising retreadable tyres

- Strengthening local retreading industries

- Reducing dependence on short-lifecycle imports

- Building resilience into supply chains

But this requires something critical: policy agility. Because if regulation lags behind market dynamics, it will not transform the system – it will merely formalise its inefficiencies.

A STRATEGIC CONCLUSION

If EPR systems are designed without properly integrating retreading – and without differentiating based on actual circular performance – they risk reinforcing a linear logic under a circular narrative. For emerging regions, this would be a critical mistake

The discussion around repair, reuse and retreading can no longer be treated merely as a waste management issue. It is increasingly becoming a matter of industrial resilience, strategic autonomy and economic security.

As global supply chains face growing pressure from geopolitical fragmentation, logistics disruptions and volatility in raw material markets, extending the useful life of products is emerging as a strategic capability for nations and industries alike.

In this context, Right to Repair should not be understood only as a consumer right but also as an industrial policy tool capable of strengthening local economies, reducing external dependency, preserving technical capabilities and supporting more resilient production systems.

Retreading, remanufacturing and reuse are part of a broader transition where value creation is no longer based exclusively on extraction and disposal but increasingly on intelligence, efficiency and lifecycle management.

CIRCULARITY WITHOUT HIERARCHY BECOMES INEFFICIENCY. REGULATION WITHOUT DIFFERENTIATION BECOMES DISTORTION.

Final note

The future of the tyre industry will not be defined only by how we recycle, but by how intelligently we extend the life of what we already produce. And that requires alignment between:

- Industry dynamics.

- Policy design.

- And strategic vision.

In that equation, retreading must move from the margins to the centre. Because properly understood, it is not just a process. It is a strategic filter, an industrial policy tool and a geopolitical lever.

- Association of Natural Rubber Producing Countries

- ANRPC

- Natural Rubber

- Monthly NR Statistical Report

ANRPC Publishes Monthly NR Statistical Report For May 2026

- By TT News

- June 30, 2026

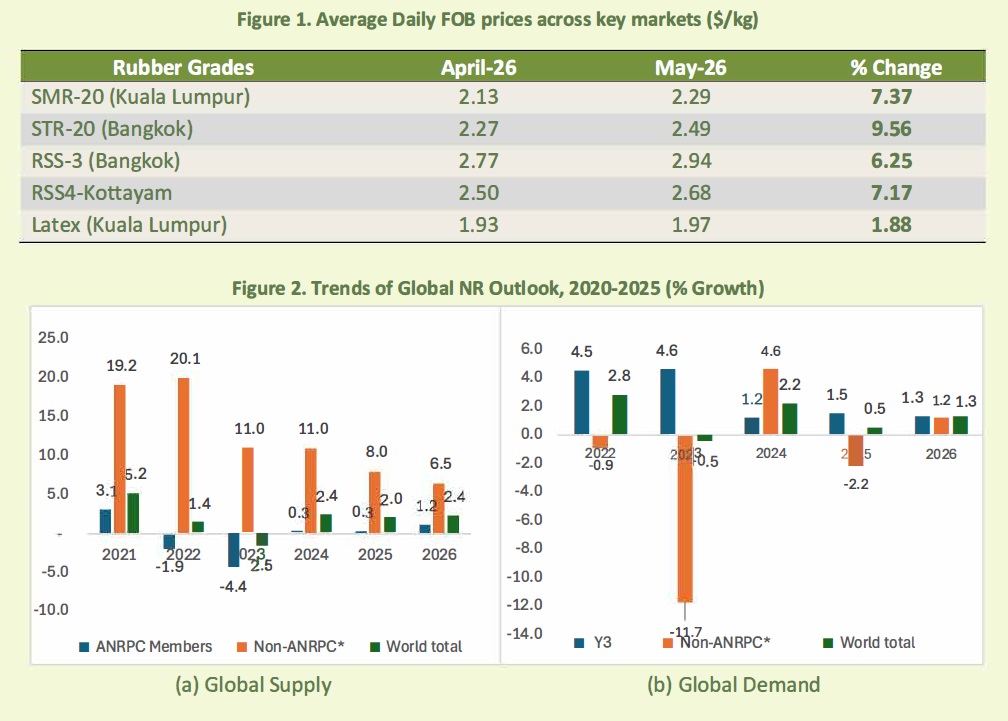

The Association of Natural Rubber Producing Countries (ANRPC) has released its market report for May 2026, depicting a sector characterised by sustained price strength and firm fundamentals. The global natural rubber market received additional upward momentum from a decline in Brent crude oil prices, which averaged USD 107.14 per barrel during the month. This represented a month-on-month decrease of 8.65 percent, attributed to easing geopolitical tensions in the Middle East and the temporary reopening of the Strait of Hormuz, which collectively bolstered the commodity's outlook.

Global production projections for 2026 stand at 15.337 million tonnes, marking a 2.4 percent increase from the previous year, with growth driven by Thailand, China, India and Malaysia, even as output moderates in Indonesia and Vietnam. Monthly production, however, fell to 997,000 tonnes in May, a year-on-year decline of 4.7 percent, due to seasonal wintering and dry weather conditions across South and Southeast Asia. Concurrently, worldwide consumption is forecast to rise by 1.3 percent to 15.550 million tonnes for the year, with May's consumption reaching 1.310 million tonnes, a 4.6 percent annual increase. This demand was underpinned by steady tyre manufacturing, electric vehicle-related consumption and resilient purchasing managers' indices in China and India, alongside record auto retail sales in India.

Physical prices for all major grades recorded broad-based gains throughout May, with SMR-20, STR-20, RSS-3, RSS-4 and latex all experiencing increases. Trade flows showed a mixed pattern, as imports from China and India contracted month-on-month, while Malaysia and Vietnam registered significant gains. On the export front, Cambodia, Vietnam and Thailand recorded increases, whereas Indonesia and Malaysia saw declines. Currency movements saw the Malaysian ringgit ease slightly, while the Thai baht traded within a stable range, and both nations reported decelerating GDP growth for the first quarter of 2026. Futures contracts on the SHFE and SGX reflected tightening supply and firm demand, posting notable month-on-month gains.

The market outlook remains cautiously balanced against a backdrop of several macroeconomic factors. Elevated trade tensions between United States and China, ongoing geopolitical conflicts and a steady United States Federal Reserve interest rate policy present potential headwinds. However, these are being offset by supportive elements, including the accelerating adoption of electric vehicles, tight feedstock supply due to adverse weather and the positive market sentiment generated by the European Union's decision to lower anti-dumping duties on Chinese tyres.

- Zeon Corporation

- Rubber Product Development

- Elastomer Research and Development

- Data Management System

Zeon Debuts Centralised Data Platform To Streamline Rubber Product Development

- By TT News

- June 29, 2026

Zeon Corporation has introduced a novel data management system specifically designed for elastomer research and development, marking the company’s first foray into a subscription-based service model. The platform is engineered to centralise and streamline R&D data pertaining to rubber products, with the primary goal of enhancing operational efficiency and accelerating developmental processes for its clientele. The initial phase of the rollout will concentrate on the Japanese market, with a strategic plan to broaden access to other regions in the future.

The elastomer industry frequently grapples with the fragmentation of data across disparate systems, which complicates the effective utilisation of historical information. Through extensive experience in elastomer supply and sustained client engagement, Zeon has identified this operational hurdle as a pervasive issue affecting the entire sector. This recognition has been the catalyst for developing a solution that directly confronts these data management deficiencies.

The newly launched system incorporates specialised functionalities that are finely attuned to the nuances of rubber product R&D. It integrates a comprehensive database that combines master data for key compounding agents available in Japan with extensive catalogue information, facilitating rapid and efficient data access for daily research tasks. The platform’s intuitive interface and user experience are meticulously crafted to optimise usability and data visualisation, with a commitment to ongoing enhancements based on evolving customer requirements.

Zeon has formally designated this data management solution as a growth driver for its strategic initiatives, extending beyond the Phase 3 objectives of its STAGE30 medium-term plan. The company envisions this business becoming a cornerstone of its strategy to augment the value proposition of its elastomer operations. By synergising its deep-seated elastomer expertise with advanced data utilisation technologies, Zeon is poised to foster innovation in client R&D and propel the overall advancement of the elastomer industry.

A new bio-based cut & chip resin for the most demanding applications.

NaugaShield BIO-TR 30 is SI Group’s latest advancement in bio-based performance resins designed to significantly improve cut and chip resistance in high-severity rubber applications. With approximately 75 percent bio-based content, this innovative material delivers on sustainability targets while exceeding the performance typically associated with petroleum-derived resins, making it a strong choice for applications such as OTR tyres in mining, construction and agriculture, mining conveyor belts, rubber tracks and mill linings.

Cut and chip resistance is a complex set of material behaviours, including static mechanical strength, dynamic response under deformation and ability to withstand sharp impacts and abrasive environments. In demanding applications such as mining or agriculture, materials must tolerate repeated high-strain loading and resist the initiation and propagation of tears. NaugaShield™ BIO-TR 30 was developed precisely to meet these conditions, demonstrating notably low dynamic heat buildup and excellent tear strength – characteristics closely tied to enhanced cut and chip resistance and long-term durability under cyclical loads.

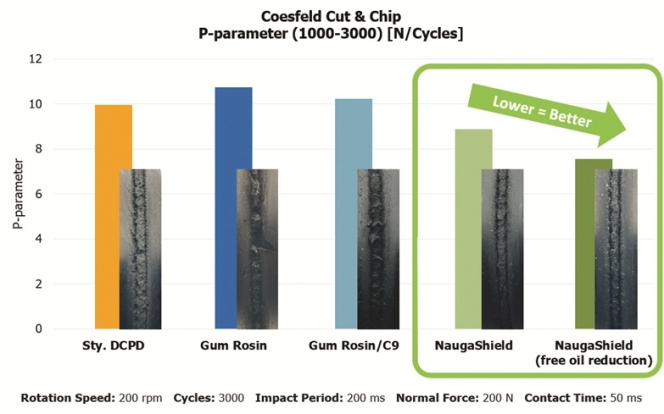

To evaluate its performance, NaugaShield BIO-TR 30 was benchmarked in an Off-road Rib Tread formulation against two widely used industry references: a gum rosin/semi-aromatic C5/C9 resin combination and a styrenated DCPD resin. All materials were tested at an equal loading of 10 phr to provide a direct and unbiased comparison. Under these conditions, the bio-based resin consistently outperformed both alternatives, offering a stronger balance of reinforcing behaviour, improved tear propagation resistance and superior resistance to thermal degradation during dynamic flexing. Further improvements were achievable by reducing the amount of free extender oil in the compound, underscoring the resin’s adaptability in formulation design and its ability to unlock even greater performance when optimised.

These laboratory indicators were corroborated through extended Coesfeld Cut & Chip testing (see chart), in which compounds were subjected to up to 3,000 cycles at 200 rpm under a 200N applied force. Formulations containing NaugaShield BIO-TR 30 exhibited substantially lower mass loss and maintained tread surface integrity more effectively than the hydrocarbon and gum rosin-based-benchmarks. The performance advantage was even more pronounced in compounds adjusted for lower free oil content, confirming that the resin can be tailored to meet the durability requirements of the most challenging operating conditions.

The strong performance of NaugaShield BIO-TR 30 in OTR tread compounds can be readily transferred to other rubber goods that encounter similar wear mechanisms. Applications such as mining belts, agricultural and construction tracks or mill linings benefit from the resin’s ability to reinforce the rubber matrix, reduce crack growth under repeated impact and maintain structural cohesion under high-strain deformation. This versatility allows manufacturers to integrate a 75 percent bio-based resin that supports sustainability by reducing fossil-based content and helping end products last longer while maintaining – and often improving – operational performance across multiple product lines.

NaugaShield BIO-TR 30 is currently available in commercial quantities, enabling compounders and manufacturers to move directly from laboratory evaluation to pilot- and production-scale trials.

Comments (0)

ADD COMMENT