- Tata Motors

- Tata Power Renewable Energy Limited

- EV Charging Solutions

- EV Charging Points

- Electric Vehicles

- Commercial Electric Vehicles

Geared up for youthful future

- By 0

- April 26, 2020

By Sharad Matade

TVS Eurogrip is geared up to lead customers into the future of riding, with its range of technologically advanced and high performance tyres, says V. Sivaramakrishnan, Chief Technology Officer

V. Sivaramakrishnan has been in the corporate sector for over 25 years. Currently he is the Chief Technology Officer at TVS Srichakra Limited, Madurai. He had earlier worked with JK Tyre and Continental Tyres. He was instrumental in leading the key strategic initiatives that has propelled the business to its new heights. His ability to lead the vision and execute it impeccably has helped the organisation grow globally. He spoke to Tyre Trends on the leading two-wheeler tyre maker’s future vision

Q: Last year TVS Srichakra launched the TVS Eurogrip brand. With this launch, the company is bringing out a completely new range targeting Y-Gen. Going forward, what will be the impact the millennial customers on the Indian two-wheeler tyre industry and the company. How do you see the tyre markets for lower CC bikes/ commuting bikes?

.jpg)

A: We believe that our brand is not just a logo, but represents who we are in terms of technology, quality and performance. We are a leader in the two-wheeler tyre space. In the last three decades since our inception, our brand has retained its core values of trust and reliability. Over the years, we have continuously evolved ourselves and our offerings by listening to the voice of the customer. Our most recent and extensive research shows a further evolution of the needs of our customers. The two-wheeler tyre space is seeing the rise of the consumer who looks for technology led products which help them outperform in multiple dimensions of life. The new age rider of today wants to live every moment to the fullest, impress his peers, and go beyond the normal. As our consumers are becoming more aspirational, we have designed our products to be the partner in their journey.

The brand idea of TVS Eurogrip - Outlive, Outperform and Outdo - is based on this insight. In anticipation of this changing tide, we are geared up to lead our customers into the future of riding, with our range of technologically advanced and high performance TVS Eurogrip tyres.

We are also going to launch a range of specialist products under the TVS Eurogrip brand. These tyres are: Designed and developed, not just for the Indian market but for the global market.

Tested extensively at our unique test track in Madurai as well as test tracks in Europe, by expert test riders from India, Japan and Europe

Manufactured at our state-of-the-art factories in Madurai and Pantnagar

Lower CC bikes for commuting will continue to remain the main segment in India. Over time, youth will be the dominant consumer base in the segment as well. Thus, it is imperative to meet their aspirational needs through innovative products, at competitive prices.

Q: The 2-W tyre market is already crowded and has stiff competition. How does the company plan to be the market leader in the segment?

A: We are a specialist in the two-wheeler tyres. The technology and expertise required in two wheelers is significantly different from four wheelers. This focus has made us one of the leading manufacturers across the globe for two-wheeler tyres. With the TVS Eurogrip brand we are looking to offer next generation products to our consumers.

Over the years, TVS Srichakra Limited has been expanding its footprint and outperforming itself by adopting cutting-edge technology driven by state-of-the-art research and development with experts in India and overseas. Under the TVS Eurogrip umbrella, we are going to launch a portfolio of 19 premium tyres that include industry leading zero-degree steel belted radial tyres. These extreme performance tyres will provide unmatched stability at high speeds and are rated to run at speeds up to 270kmph.

Q: Continuous Improvement in production efficiency is something the industry is talking about. What efforts are being taken in this direction for both of your plants?

A: We are the first tyre company in India to have achieved TPM excellence for our Manufacturing processes. We continue our efforts and have embarked on TQM journey. We have established state of art manufacturing facilities with modern mixing, calendaring plant and world class Radial tyre plant. Connected and Intelligent Manufacturing Systems are the future and we are not behind in this journey. We have commenced a project to implement Industry 4.0 concepts for our existing plants.

Q: How do you distinguish OE and aftermarket? What are your strategies to expand your share in the aftermarket, where price pressure is imminent?

A: Like our OEM business we are also witnessing superior growth in the aftermarket. We have a strong 2000 dealer network spread across the country which is assisting us in expanding our domestic presence. We are working to add new dealers and channel partners to maintain our growth in the aftermarket. Deeper penetration and reach have been our biggest strength and will continue to contribute to our strategy to tap the aftermarket.

Q: In OTR tyre segment, 90% of your business comes from export. What are the new trends you see in the segment? Any plans to focus on the domestic market?

A: We currently export to over 70 countries, including Europe. Our exports are largely Off-Highway tyres and we have gained expertise in making tyres of different sizes and quantities. We are also ensuring that cost of carrying inventory for the distributors is the lowest. We continue to seek opportunities in international markets and have invested in Technology and R&D to design and develop, not just for the Indian market but for the global market. This should significantly assist us in foraying further into the international markets.

Q: Safety is a crucial factor, especially in two-wheeler tyres. What technical and material developments are happening to improve the grip of two-wheeler tyres?

A: Our research programs are focused on maximising vehicle handling performance and tyre grip on wet and dry surface. We have developed some of the finest materials applying nano science to enhance the grip properties. We have invested in a state-of-the-artstesting facility, which includes a modern test track in Madurai, home for our R&D Centre.

We have started a Technical Cetre in Milan, Italy where experts focus on research programs of high-performance tyres for India and global markets. A host of new patterns are under development in this centre aimed at delivering high grip performance.

Q: We may see electrification in three-wheeler segment soon. How are you preparing yourself for this as you also produce three-wheeler tyres?

A: The advent of EVs does not do away with the need for tyres. Being a 2W and 3W tyre specialist, we are geared up for any advancement that is called for as the industry evolves.

Q: What about production capacity, utilisation rate, and export volume? What are your expansion plans?

A: We produce about 34 million tyres per annum and have made significant investments to capture market opportunities. We will continue to invest in expansion of our capacities and capabilities in line with market dynamics, latest technology and our own growth aspirations. Currently the OEM business accounts for half of company’s sales volumes with aftermarket and export market contributing the other half for the company. We want to expand our reach i.e. enter newer markets and improve our volumes from the markets where we are currently present.

ENDS

The Gulf Crisis Leading To A Profound Change In The Tyre Industry

- By Ertugrul Bahan

- June 15, 2026

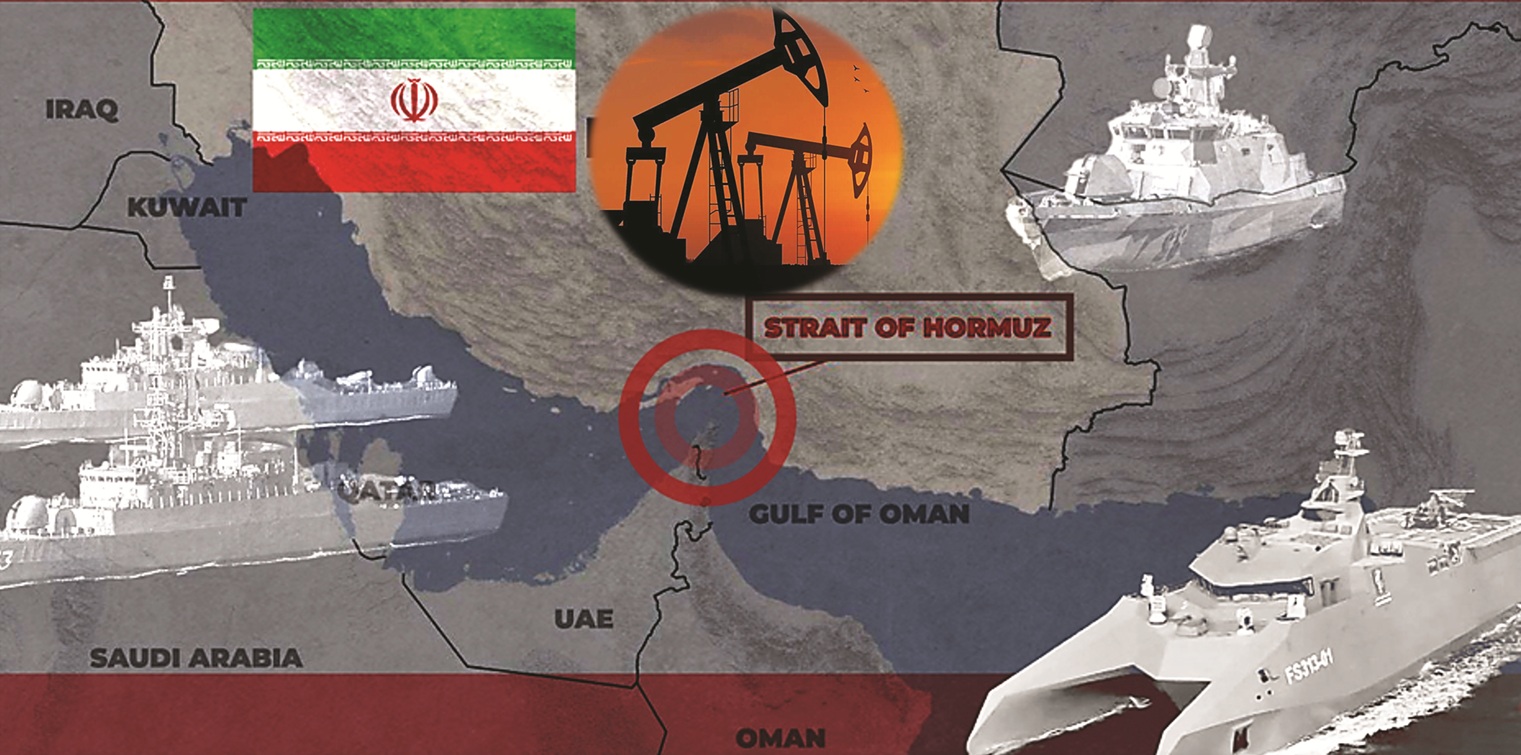

The effects of the Strait of Hormuz closure will become particularly evident in 2026 and undoubtedly represent a strategic bottleneck for global energy and petrochemical trade. The Gulf War disrupted raw material supplies, crippled logistics and destabilised key export markets.

While the war represents a financial catastrophe, it also presents new opportunities. It has driven up raw material costs, while the logistics crisis has impacted export markets. The financial consequences include shrinking margins and reduced demand. However, long-term strategic shifts are expected, and these trends are likely to accelerate by 2040.

The closure of the Strait of Hormuz and the disruptions in the Red Sea have brought maritime traffic to the Middle East and Europe to a near standstill. The war has caused logistical chaos, and exports face immediate difficulties. China alone was expected to export more than seven million tyres to the Middle East by 2025, but this vital trade route is now blocked by skyrocketing freight rates and insurance premiums.

The profitability of the sector, whose gross margins are expected to fall to slightly more than four times their pre-war levels, is likely to be impacted by market consolidation and rising demand for high-tech tyres, particularly for electric vehicles. In the short to long term, the costs of raw materials such as synthetic rubber, carbon black and logistics are expected to rise significantly. Furthermore, this crisis could spur massive investments in bio-based and recycled materials to reduce dependence on petroleum. To address supply bottlenecks, the sharp decline in exports from the Middle East, coupled with significantly increased transportation costs, should be offset by regionalised production, for example, in India and Southeast Asia. With regard to product development, the short-term priority of cost control should lead to an acceleration of research and development into sustainable rubber compounds and sensorless smart tyres.

The end of the Gulf War is likely to usher in a period of weak economic growth and high inflation. The tyre industry is already facing a profound restructuring process. In the post-war era, the focus is not only on repairing the damage but, above all, on accelerating the long-term transition to regionalised supply chains, a circular economy and value creation through technology.

The most immediate consequence of war is a drastic increase in raw material costs,

which can account for almost 70 percent of tyre production costs. Around 45 percent of the raw materials used in the tyre industry are petroleum-based, and another 45 percent are natural rubber. In the case of synthetic rubber (NBR/SBR), the direct rise in oil prices leads to a price increase for butadiene, a key raw material. In the US, NBR prices rose by 7.4 percent at the beginning of March 2026; in China, butadiene prices jumped by 25 percent within a week.

Analysts estimate that this conflict could reduce global natural rubber production by 36 to 45 kilotonnes in the first half of 2026. How can this be explained, given that the effects on natural rubber are indirect? Diesel shortages prevent trucks from collecting rubber from plantations, thus reducing supply on the market. This shortage is contributing to the energy crisis in Southeast Asia. Prices for carbon black and chemicals derived from oil and gas are also rising in line with increasing energy costs. The supply of speciality chemicals (such as bromine from Israel) is also at risk.

Bio-based materials, particularly long-term ESG pilot projects, represent an immediate strategic necessity. The market for bio-based materials is projected to reach USD 337 million by 2032, with a compound annual growth rate (CAGR) of 101 percent, thus replacing volatile petrochemical feedstocks. Similarly, it is becoming increasingly clear that tyre pressure monitoring systems (TPMS) and sensorless, AI-powered systems like Michelin SmartWear can reduce costs and enhance safety.

Rising energy prices and crumbling infrastructure will weigh on consumption and investment. Inflation is high and is expected to remain high (around four percent for the G20 in 2026). Even after the war, energy costs and the rebuilding of supply chains will keep prices high. Consequently, the post-war economic recovery is expected to be slow and uneven, without a V-shaped rebound. The war has left lasting scars on global supply chains and public finances. Global GDP growth is weaker and below the pre-pandemic average.

In the field of carbon black recycling, carbon black is developing into a strategic raw material. Recycled carbon black (rCB) and tyre pyrolysis oil are becoming strategic raw materials intended to replace unstable fossil fuels. Massive investments, such as in Lummus-InnoVent, a continuous pyrolysis technology, will increase rCB production and reach a market of USD 15.6 billion by 2034.

Sustainable and bio-based materials are of great strategic importance, and significant investments are already being made to increase their production. Rising oil prices are making bio-based alternatives economically viable and essential for security of supply. Therefore, the transition to sustainable materials is no longer just an ESG goal but a necessity for the entire supply chain.

The Gulf War acted as a powerful catalyst, transforming promising future trends into immediate and essential investments. Bio-based silanes, for example, are now being used more and more frequently. Momentive’s NXT P97, a next-generation silane for electric vehicle tyres with 79 percent bio-based carbon, reduces reliance on fossil fuels while improving rolling resistance and durability. This technology, a prime example, is currently being deployed on a large scale.

The Gulf War acted as a powerful catalyst, transforming promising future trends into immediate and essential investments. Bio-based silanes, for example, are now being used more and more frequently. Momentive’s NXT P97, a next-generation silane for electric vehicle tyres with 79 percent bio-based carbon, reduces reliance on fossil fuels while improving rolling resistance and durability. This technology, a prime example, is currently being deployed on a large scale.

Tyre prices will remain high. The recovery will therefore be characterised more by rapid strategic development than by a simple return to pre-war levels. It is not so much the fluctuating demand from car manufacturers, but rather the replacement tyre market, which alone accounts for 70 percent of the volume, that is likely to continue to strongly support the consumer goods and logistics sectors during the economic recovery.

Increasing uncertainty is becoming the new normal. Geopolitical risks remain a key concern, forcing companies to prioritise resilience over efficiency. This situation is creating unequal competitive conditions for tyre manufacturers and their core markets. The difficulties faced by energy-importing countries in Europe and Asia will be further exacerbated in this climate of uncertainty.

This crisis will be one of the main reasons for the relocation of production to key markets, forcing the tyre industry to make unavoidable investments. It will be compelled to implement the technologies necessary for a more resilient, sustainable and technologically advanced future. New production centres will be established to circumvent geopolitical obstacles. This new dynamic is characterised by a clear strategic realignment of production and supply chains, accelerating ‘out-of-China’ models and leading to regionalisation. This conflict is not merely a disruption but a form of brutality for economically weaker countries, even if it represents a highly effective response to the relocation of production areas.

This war teaches us that excessive dependence on unstable regions like the Middle East must be balanced by the need for market diversification. Exporters like China and India will increasingly focus on Africa, Latin America and Southeast Asia. Margins will remain under pressure in the short term. High raw material and energy costs will not fall immediately. Large global companies will gain market share by leveraging their size and technology, as well as through increased regionalisation. Conversely, smaller, less diversified companies risk being acquired or exiting the market. Companies with strong pricing power and high operational efficiency will recover faster than those that rely solely on low prices.

The tyre industry is facing profound change. The tyre market is being restructured, and local, sales-oriented production is being intensified to circumvent geopolitical barriers and tariffs. In the short term, demand is expected to recover, but profit margins will be severely impacted by persistently high costs. In the long term, the sector will become more regionally focused, evolve towards a circular economy and rely more heavily on technology. In short, the end of the war will not restore the pre-conflict status quo. The crisis has forced a difficult but necessary transition to sustainable and resilient business models that will shape the key trends through 2040.

Fifty-seven years ago on 1st September 1968, I joined the rubber products manufacturing industry in Sri Lanka (then Ceylon) as a trainee in a medium scale footwear company. The only knowledge or rather awareness I had of rubber until that time was seeing the tapping of trees, adding a pungent liquid to the milky liquid, put on metal trays, squeezing the whitish slab of material through two rotating metal rollers manually rotated by a crank and putting them in a smoke shed that was available in some backyards to end up with a striped brownish sheet of rubber, which I later learnt was known as RSS. Later, in the early sixties, during our Organic Chemistry lessons, we learnt that C5H8 is the formula for Isoprene, which is the building block of natural rubber. Going down the memory lane of the past 57 years of knowledge acquisition in the rubber industry might turn out to be an exhaustive exercise. However, it is my sincere hope that some of my experiential insights might help the modern-day managers to seek areas that may strengthen their foundations in this era of rapid shifting sands.

I should say I am at a loss in finding an appropriate definition of knowledge from the vast interpretations which appear to be too academic. One practical and easy to understand definition I have come across in that knowledge is the ability to understand, apply and transfer information and experience to solve problems and adapt to changing circumstances, Merely the possession of facts is meaningless. It is the skill of using them effectively for survival, development and progress that is more important. It reminds me of the many research findings and innovations that are gathering dust in many institutions. In the case of early humans, knowledge emerged through direct observation of nature, trial and error and sharing same with groups. In my opinion, the context has virtually been the same over the ages, although the scope and the contents have undergone drastic changes during the course of human history, particularly through the four industrial revolutions and apparently heading for an unprecedented and a somewhat incomprehensible future.

If I am asked the question how I have acquired knowledge during my working life, I would say without any hesitation that it was through a process of osmosis. Those who studied botany under the biological sciences may perhaps vaguely remember how plants absorb water, minerals and other nutrients from the surrounding soil through their root systems by the process called osmosis. In a similar manner, we also acquire knowledge from the external environment through our sense facilities, namely the eyes, ears, nose, tongue and the skin, and through perceptions, which are processed by our brain and the central nervous system. The Buddhist doctrine gives a clear description of this process, which are well in line with the biological and physiological sciences. I, however, would not wish to go in to a philosophical deliberation at this point of time. Knowledge acquisition is a lifelong process with the ‘cradle to grave’ concept, and according to the modern scientific findings, starting at the moment of our conception in the mother’s womb.

I would now endeavour to delve a little into the knowledge acquisition modalities available to us trainees during our formative days of the career in the rubber industry from the late sixties onwards. The modern rubber technologist (if the term is still in use) may perhaps find them archaic as if they are viewing the archaeological remnants exhibited at a museum. It was hands-on experience from the beginning in what was termed a 3D industry, namely dirty, difficult and dangerous. This was mainly due to the particulate and dusty nature of the various fillers used such as carbon black and the toxicity of the rubber chemicals, coupled with the usage of high energy consuming motor driven machinery, both electrical and heat, usage of steam and compressed air, emission of high noise and vibration, fumes and high material load in some industries such as tyre manufacturing and tyre re-treading. The complexity and diversity are further aggravated by the macromolecular nature of both natural and synthetic rubber, which necessitates the somewhat illogical steps of breaking and remaking using a vast array of heterogeneous raw materials to facilitate the processability and for achieving the performance requirements of the products, some of which are of highly composite nature. As a consequence of the above, rubber product manufacturing industry was not at all the preferred choice for young school leavers like me. Hence, my entry into the rubber industry was due to the pure necessity of finding employment. However, the practical involvement with the identification and weighing of the multitude of rubber raw materials somehow had its attraction for me, which prompted me to read the limited number of text books and supplier literature that were available at that time. The real turning point in my career in the industry was the opportunity I got to follow the two-year part-time course at the then Ceylon College of Technology (now a university) to study for the Licentiate of the Institution of the Rubber Industry, LIRI (UK). This was equivalent to a full time BSc today. We were very fortunate to have three well-respected and dedicated teachers of the day in our quest for the acquisition of knowledge. Teaching was a noble profession for them, and I am very proud to state that their photographs adorn the entrance to the auditorium at the Plastics and Rubber Institute of Sri Lanka, where I joined as student in 1969 and ended up as its President for the year 2024.

Another remarkable feature during those days came in the shape of representatives from well-reputed giants in the raw material manufacturing companies such as Bayer, ICI, Monsanto, ACCI Rhien-Chemi and Polysar, names which to my knowledge are not existing now, or may be as mergers. These were invaluable opportunities for us the young technologists to gain the technical knowledge and discussion about the technical problems. The short technical sessions conducted by some of them in the evenings were eagerly awaited occasions during our days to share knowledge over a cup of tea. I am a little puzzled whether some of the similar events conducted online as webinars have the same effects or if at all that personal rapport.

The Bayers Technical Programme conducted annually at Thane, India, during those days was another avenue for gaining very valuable theoretical and practical knowledge, and I was fortunate to associate with prominent professionals such as R R Pandit, who left this world a few years ago, and Dr S N Chakravarthy.During my working with the Bata Shoe Company of Ceylon for 12 years, I had the opportunity to represent the company at a few of the Regional Technical Meetings held in the Far East. These were invaluable platforms for sharing knowledge and information of the technical developments of the individual companies. They were also enjoyable opportunities for networking and building up some lasting relationships. After following the programmes, it was compulsory that we give a presentation to the management and staff about our learning experiences, and more importantly, to plan development activities, the success of which was one criterion for our individual performance evaluation. Knowledge by itself is not power unless it is shared – a truism that will not apply to politics and the intelligence services. I well remember the case in a place I worked later about how some staff members who were sent to Japan for training deliberately skipped sharing what they learnt at company expense with the fellow staff members despite the several reminders.

As a passing remark, I may mention that my period of working in the tyre retreading and rubber products manufacturing companies in Kenya (for about 14 years) offered me the good opportunity of working with multiethnic communities while imparting my knowledge to train and develop staff members.

Now, coming to the global rubber product manufacturing, it can be seen that the focus on mixing, curing and reinforcement knowledge requirements has expanded into a multidisciplinary portfolio over the past 50 years, and the quest will continue. It is not prudent to do comparisons as ‘now and then’ because knowledge acquisition and its management is heavily dependent on the needs and requirements at any particular era or period of time. Unlike in our generation, a vast knowledge base, which is sometimes bewildering, is available at the touch of a fingertip for the modern-day managers, and apparently, most of it is related to their work and operational activities. My discussions and chats with many managers reveal the fact that they are overburdened with their daily activities and are working at different stress levels. They seldom seem to have any time or opportunity to integrate their work with the core values such as respect, gratuity and empathetical understanding.

The famous quote of Sir Issac Newton comes to my mind at this juncture: “If I have seen further, it is by standing on the shoulders of Giants.” He wrote this statement in a letter to Robert Hooke in February 1675, acknowledging that his own scientific discoveries were built upon the work of his predecessors, a sentiment that symbolises humility and scientific progress.

Knowledge and discipline go hand in hand. How to use knowledge appropriately needs discipline to comprehend. The consequences of using knowledge for the sake of knowledge, purely for application to industry, without giving due recognition to humanity and our core values is surfacing rapidly at the cost of trust, wellbeing, harmony and human development in every aspect of human activity, both locally and globally. In this respect, I remember the famous line from the poem, The Rime of the Ancient Mariner, by Samual Taylor Coleridge, which we happened to study in our literature class a long time ago.

‘Water, water everywhere and not a drop to drink’ illustrates the irony and anguish of being desperately hot and thirsty whilst being surrounded by nothing but ocean.

The author is a Management Counsellor from Sri Lanka.

Service is being there to assist the client to experience less lost profit. Some may say pain; obviously, of the financial kind and not physical kind.

Navigating life’s challenges becomes considerably more complex when a flat tyre comes into play. Preferably first thing in the morning, as the tyre’s lost its pressure over night. The tyre wasn’t capable of delivering its usual level of service when you required it to do.

A tyre service delivery has the client’s wellbeing in mind when managing the usually large asset for a fleet operation that is known as ‘TYRES’. From initial selection through procurement service and end of first life, decisions are required based on experience, knowledge and data. Supply alone cannot support such an operation requiring service to monitor, measure, maintain and manage tyres in operation. In a round the clock operation, tyres don’t just operate on one shift.

Electronic surveillance is becoming part of daily life, no different for tyres. Uninterrupted service, but can you can stay awake long enough?

What has changed is the service a tyre now receives from tyre pressure monitoring. Operating at the appropriate pressure, a tyre can deliver the highest level of service it is capable of. The service provider now becomes the service receiver. Indeed, both are becoming the service controller with the delivery of smart tyres. The tyres provide service to the control systems of the vehicle, updating on current conditions and even considering what is to be experienced based on what the tyres are feeling, just as a human does, in delayed response.

THE SERVICE LOOP CLOSES.

Good service always should breed trust and respect and so loyalty. Unfortunately, sometimes prices come into play. As our industry knows only too well, quality is never (ever) low cost. If it’s too good to be true, it probably is. Is your (or someone else’s) life worth a fist full of money? Bean counters have a lot to answer for when it comes to tyre operations.

Service is supporting your client to assist them to generate a profit. Would you turn away someone who helps you make money? So how do we assist to reduce the pain point? Real-time tyre pressure monitoring, know the issue before it becomes a problem, before the hazard threshold is crossed. With ease data can be streamed in real time. A tyre service centre is able today to alert a fleet operator that a tyre is in need of attention, before the situation develops into a catastrophic tyre failure. The nearest service facility can be alerted, the vehicle with the problem tyre already known to the service facility is attended to and returned to service. The service loop closes again. The tyres assist you making a profit, ergo a service provider.

Someone or something that makes my life better is to me a service provider. I consider that a reflection of the trust a client invests in their supplier to be a prime indicator of the level of service that is utilised. There are times when service is ridden rough shod over as price becomes the primary driver. Service suffers, returns from the tyre operations fall as tyre costs rise, though more importantly, machine availability drops. Remember, the sweet low price is long forgotten when low quality is found.

What is your level of service to your clients? Will they return to you or go looking elsewhere?

Our tyres rarely complain and endure the harsh conditions we ask them to operate in, without attention and generally without any care.

Remember the level of service your tyres provide to you and yours. Can you emulate this level of service provision to your clients, friends and family?

Take care, stay TyreSafe!

Driving Forward Through Uncertainty

- By Rajiv Budhraja

- September 04, 2025

The past few years have not been easy for Indian industries. From post-pandemic recovery and supply chain issues to trade policy shifts and geopolitical conflicts, businesses across sectors have been navigating uncertainty. Yet, amidst this turbulence, the Indian tyre industry is emerging resilient – steadily carving out a global presence and positioning itself as a poster boy of India’s manufacturing story.

In the last one month alone, three developments have highlighted the strength, adaptability and future-readiness of the Indian tyre sector. Together, they offer a glimpse into an industry not only responding to challenges but also reimagining the road ahead.

Despite rising protectionism and the lingering aftershocks of disrupted global supply chains, Indian tyre exports have continued their upward march. In the last fiscal year, tyre exports from India have grown by nine percent year-on-year – a clear indication of global confidence in Indian-manufactured tyres. Tyre exports from India reached INR 250.51 billion compared to INR 230.73 billion in the previous fiscal, as per data released by the Ministry of Commerce, Government of India.

This isn’t just a story of volume. It’s a story of credibility – built on strong domestic manufacturing capability, world-class quality standards and a heightened focus on research and development.

Today, Indian manufactured tyres are competing with the best on parameters of performance, durability and cost-efficiency and providing a value proposition difficult to match. Indian tyres are exported to over 170 countries, with significant presence in the United States, European Union, Latin America and Southeast Asia. The US remains the top export destination, accounting for 17 percent of India’s tyre exports by value, followed by Germany (six percent), Brazil (five percent), UAE (four percent) and France (four percent).

With an estimated annual turnover of INR 1 trillion and exports exceeding INR 250 billion, the Indian tyre industry stands out as one of the few manufacturing sectors in the country with a high export-to-turnover ratio.

This export momentum has been further facilitated by the government’s active support in promoting domestic manufacturing through Make in India and other export-enabling reforms.

Perhaps nothing captures the maturing of the Indian tyre industry better than the recent global rankings by Brand Finance, the world’s leading brand valuation consultancy, which features four Indian tyre manufacturers – MRF, Apollo, CEAT and JK Tyre – among the world’s 15 strongest tyre brands. In fact, MRF, with a Brand Strength Index (BSI) score of 83.5, ranks as the third strongest tyre brand in the world after Michelin and Goodyear, according to the Brand Finance report.

This is not mere symbolism. It reflects decades of effort in building product trust, expanding global footprints and investing in brand equity. From high-performance radial tyres to off-the-road solutions, these companies are not just making tyres – they are shaping mobility experiences across geographies.

If the present is promising, the future looks even more exciting. A Vision 2047 report by PwC forecasts a CAGR of 11–12 percent for the Indian tyre industry over the next two decades. That is not just encouraging – it’s transformative.

This projected growth rides on several powerful drivers including rising demand from rural and semi-urban India, rapid growth in two-wheeler and commercial vehicle segments, a paradigm shift towards electric mobility and smart transport, greater OEM activity within India as global players deepen their localisation strategies and government policy support that encourages domestic production and discourages non-essential imports.

It’s also a growth that aligns with national priorities – self-reliance, sustainability and job creation.

India’s tyre industry is no longer playing catch-up. It is setting benchmarks. It is innovating, expanding and winning trust in markets around the world. It is making bold bets on sustainability, supply chain resilience and digital transformation. Tyre manufacturers in India have collectively invested nearly INR 270 billion over the last 3-4 years. These investments, spanning both greenfield and brownfield projects, highlight the industry’s confidence in India’s long-term growth potential and the industry’s commitment to capacity expansion and technological advancements.

As we steer towards 2047 – India’s centenary of independence – the tyre sector stands ready to play a pivotal role in the journey. One that connects not just places but aspirations.

Rajiv Budhraja is Director General of the New Delhi-based tyre industry association, Automotive Tyre Manufacturers’ Association (ATMA).The views expressed here are personal.

Comments (0)

ADD COMMENT