Elastomer Tackifiers

- By Dr. Samir Majumdar

- October 19, 2020

Elastomer tackifiers are those that produce green tack in elastomers. The term “tack” refers to the ability of two uncured rubber materials to resist separation after bringing them into contact for a short time under relatively high pressure. Building tack of rubber components is an important pre-requisite to enable tyre building on the tyre building drum where different rubber layers are put together on the tyre building drum before they are cured. Another important property of tackifier is, it should retain its tack on storage. A good tackifier, therefore, should have the following properties :

- Very high initial and extreme long-term tackiness

- No adverse effect on the rubber compound cure on scorch

- No interference on (a) rubber to metal bonding (b) rubber to fabric bonding

- Physical properties of the cured rubber remain unchanged

- No effect on the performance of aged rubber compound properties

- Improves rubber compound process reliability

- Show extreme good performance in silica / s-SBR based rubber compound.

In general, NR has enough tack because of the presence of a very high quantity of low molecular weight fraction, having its wide molecular weight distribution. Its low molecular weight fraction also generates during its break down in machines. On the contrary, synthetic rubber lack in tack property because of the absence of enough low molecular weight fraction in them, having narrow molecular weight distribute on (Fig.1). Synthetic rubber also resists in the molecular break down upon mastication and therefore, cannot produce low molecular weight fraction. Resins are typically produced with molecular weights (Mw) between 1,000 and 2,000 with maximum Mw around 3000. The molecular weight is important since tackifying resins work at the surface of the rubber compound and must be able to migrate to the surface to be effective. If the molecular weight is too low, the resin will remain soluble in the elastomer and not migrate its way to the surface. If the molecular weight is too high, the elastomer will be insoluble in the elastomer. Rubber industries use both synthetic and natural resins for tack. Following three types are in major use in the industry :

- Aromatic Resins (Phenolic, Cumaron Indane)

- Petroleum based resins

- Plant Resins ( wood rosin resins,Terpene resins)

Only plant resin is a source of natural resins. However, due to product consistency and different compatibility factors, synthetic resins are in major use. Besides tyre and other rubber applications, the major end-uses for resins are in pressure-sensitive adhesives, hot-melt adhesives, road markings, paints, caulks, and sealants. Manufacturers use hydrocarbon resins to produce hot melt adhesives (for infant and feminine) and packaging applications in addition to glue sticks, tapes, labels and other adhesive applications. All resins are sticky and because of their low molecular weight they migrate (diffuse) easily on the rubber product surface and behaves sticky and that causes tack. Tack property is apparently due to two major reasons :

- Spontaneous diffusion of molecules between two uncured rubber layers.

- Strong molecular forces resulting high degree of crystallinity

Highest level of tack in NR could be due to both the reasons, which means, NR has a high degree of crystallinity (stress induced crystallization) and it has also broad (wider) molecular weight distribution (Fig.1), so that, having plenty of lower molecular fraction can diffuse faster between two layers in contact each other. NR is reported to improve upon its tack on mastication because it generates a higher number of lower molecular weight fraction chains upon breaking down on shearing forces in machines. CR (Neoprene Rubber) shows exceptional adhesive property because it shows the highest degree of crystallinity, even much greater than NR, due to its strong intermolecular attractive force.

Honestly, NR may not require any tackifier because it has enough low molecular weight fraction of chain molecules, due to its wider molecular weight distribution (Fig.1), to be migrated on the rubber component surface and can produce enough tack. It loses its tack mostly because it might have been processed at a higher temperature and is already in the premature vulcanization stage. It can also happen due to the fact that although calendaring or extrusions were done at the right temperature stock was made before adequate cooling and thereby allowed scorching in windup liners. It also loses its tack at cold ambient temperature, in the rainy season and also if the filler level is too high or if the viscosity of the stock is substantially higher than required. However, all synthetic rubber or when synthetic rubber (SBR,BR) is blended with NR, may require to add adequate resins for compound processing.

Except C4,C5 petroleum-based resins, all other types of resins are compatible with NR and is added 1-2 phr. Comparatively C9 petroleum-based resin is better in NR. Plant-based resins are found to work better in 100% NR. When NR is compounded with synthetic rubber, the tackifier is a must and the dose could be as high as 2-4 phr depending on the content of synthetic rubber, oil and filler in the compound matrix. All synthetic rubber lag in rubber tack because, in general, synthetic rubber has :

- Narrow molecular weight distribution

- It resisting break down of molecular chains under mechanical shear

- Synthetic rubber is in very pure form

Aromatic Resins (Phenolic, Cumaron Indane) work better in SBR and BR than plant based resins. For hydrocarbon type of elastomers like butyl , halobutyl , EPM and EPDM , petroleum base resin (C4,C5) work better and usually added with 1-2 phr in the formulation, However, with a higher dose of filler, 2-4 phr tackifier could also be added.

Tackifier resins are added to base polymers/elastomers not only to improve tack (ability to stick) but it also helps in better wetting with filler. Increase in tensile strength by adding resins has been witnessed in different types of elastomers, aromatic resins have been witnessed to increase tensile strength of SBR and its blend.

Effect of Environment on Rubber Tack

The tack of a rubber article is greatly affected by environmental conditions such

as temperature, ozone level and humidity. Environment can not influence tack, however, if processed rubber compound is used with in 24 hrs. High temperature and humidity conditions have a detrimental effect on the initial tack and tack retention of an elastomer. Phenolic tackifying resins can help improve tack under these conditions, but they have their limits under extreme conditions. Superior tack retention under the influence of high humidity can be often be achieved with epoxy resin modified alkylphenol-formaldehyde polymers.

Hydrocarbon based tackifying resins are sometimes used as a low-cost alternative to phenolic tackifying resins. However, hydrocarbon resins are not as effective at maintaining tack under adverse environmental conditions, like elevated temperature and high humidity, nor do they have the same tack retention. Hydrocarbon resins however, preferred in butyl and EPDM rubber compound due to their compatibility.

Hydrocarbon resins are not as efficient as phenolic tackifying resins, and higher levels are often required to achieve the same tack. High tackifier resin levels can cause a loss in tensile strength, tear strength and, most importantly, hysteresis. In applications where these properties, especially hysteresis, are important, phenolic tackifying resins are excellent choices and should be used.

Rubber Board Extends Planting Aid Schemes At Current Rates For 2026-27

- By TT News

- May 08, 2026

The Rubber Board of India has confirmed the continuation of all existing central sector schemes for the 2026-27 fiscal year at unchanged rates. Financial aid for new planting will be restricted to estates utilising poly bag or root trainer plants sourced solely from Board-approved nurseries, with applicants required to submit the original purchase bill. This mandatory verification step aims to ensure quality and authenticity of planting materials used across the sector.

Support for rain guarding and spraying operations will be channelled exclusively through Rubber Producers’ Societies. These societies must include GST bills for all acquired materials when applying. The official timeline for submitting applications will be announced separately by the Board, giving producers adequate time to prepare documentation and coordinate with their respective societies before the deadline.

Rubber Board Calls For Marketing Graduates With Digital Skills For Temporary Engagement

- By TT News

- May 07, 2026

The Rubber Board of India has announced a temporary engagement for a young professional within its Market Promotion Division, located at the RRII campus in Puthuppally, Kottayam. The selected individual will assist with division activities and promote ‘mRube’, the electronic trading platform for natural rubber.

Candidates must hold an MBA in Marketing or Agri Business Management with computer knowledge, while skills in digital marketing, sales or market research and proficiency in English and Hindi are preferred. Applicants aged up to 30 years as of 1 May 2026, will be considered for the one-year role, which offers a consolidated monthly pay of INR 25,000.

Interested individuals should send their applications to the Deputy Director (Marketing) at the Central Laboratory Building, RRII, Rubber Board PO, Kottayam – 686009 by 19 May 2026. Shortlisted names will appear on the Rubber Board’s website with interview details, as no separate communication will be sent.

Bekaert Finalises Acquisition Of Bridgestone’s Tyre Reinforcement Plants In China And Thailand

- By TT News

- May 06, 2026

Bekaert has officially finalised its acquisition of Bridgestone’s tyre reinforcement operations in China and Thailand, after securing all necessary regulatory approvals and meeting standard closing conditions. The deal, now fully completed, marks a significant step in the Belgian company’s expansion strategy.

The transaction brings under Bekaert’s control two production facilities: Bridgestone (Shenyang) Steel Cord Co., Ltd. in China and Bridgestone Metalfa (Thailand) Co., Ltd. in Thailand. These plants specialise in manufacturing high-quality tyre cord products exclusively for Bridgestone tyres, and they will continue to supply Bridgestone under the new ownership, further deepening the longstanding partnership between the two firms.

Financially, the acquisition is expected to add roughly EUR 80 million to Bekaert’s annual consolidated sales. The EUR 60 million cash consideration for the deal was funded from the company’s available cash reserves.

Curd Vandekerckhove, CEO Rubber Reinforcement, said, “With the completion of this acquisition within our Rubber Reinforcement division, we are pleased to officially welcome the plant teams in China and Thailand to Bekaert. Our immediate focus is on a smooth transition and operational continuity while continuing to serve Bridgestone as a key strategic partner. The completion of the acquisition further strengthens the position of Bekaert in the tyre cord market, expands the global manufacturing footprint and deepens our longstanding partnership with Bridgestone. A long-term supply agreement ensures continued delivery of high-quality tyre reinforcement within a trusted supplier model.”

- Association of Natural Rubber Producing Countries

- ANRPC

- Natural Rubber

- Monthly NR Statistical Report

ANRPC Publishes Monthly NR Statistical Report For March 2026

- By TT News

- May 06, 2026

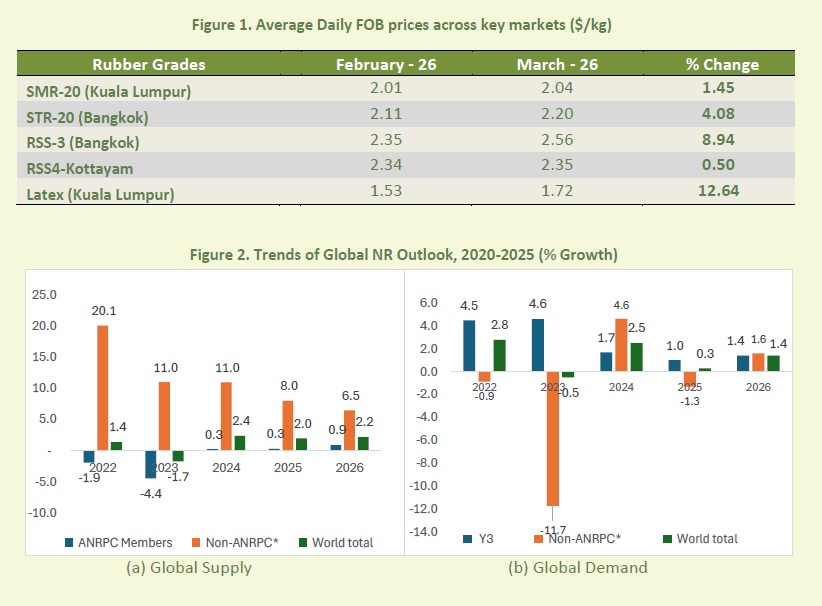

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly NR Statistical Report for March 2026, revealing a market that turned external pressures into clear price gains. While February had hinted at shifting dynamics, March provided proof of the industry’s core strength, with prices rising across all major grades and trading hubs despite an unusually challenging global environment. A 3.4 percent drop in monthly output and a dramatic 42.51 percent spike in Brent crude prices allowed natural rubber to advance rather than retreat.

Benchmark grades recorded widespread increases. In Kuala Lumpur, SMR-20 reached an average of USD 2.04 per kilogramme, while Bangkok saw STR-20 climb to USD 2.20 and RSS-3 jump to USD 2.56 per kilogramme. Kottayam’s RSS-4 averaged USD 2.35, and centrifuged latex in Kuala Lumpur rose sharply to USD 1.72 per kilogramme. Futures markets echoed the trend, with Shanghai’s May contract averaging CNY 16,662 per tonne and Singapore’s June contract closing at USD 1.95 per kilogramme.

The supply situation tightened considerably. Global March production is forecast at 786,000 tonnes, with Thailand’s output falling to 164,000 tonnes as southern growing regions endured temperatures of 42 to 43 degrees Celsius and rainfall up to 69 percent below normal levels. These punishing conditions sent a clear message that the market can absorb demand without chaotic price swings, a sign of a maturing commodity sector.

Demand told a similarly positive story. China’s natural rubber consumption surged from 446,000 tonnes in February to 610,000 tonnes in March, supported by a manufacturing PMI of 50.4, a 74.4 percent monthly rise in vehicle output, and a 130 percent annual leap in new energy vehicle exports. Chinese imports jumped 39.03 percent month-on-month to 629,800 tonnes, while Vietnam, Malaysia and Thailand boosted exports by 47.34 percent, 13.73 percent and 8.3 percent, respectively.

The oil market further strengthened natural rubber’s competitive edge. With Brent crude averaging over USD 101 per barrel and peaking at USD 126.69 on 31 March, synthetic rubber became significantly less cost-effective, giving tyre makers a strong incentive to favour natural rubber. Policy moves also bolstered confidence, including Malaysia’s replanting aid increase to RM 20,000 per hectare and a new Indonesian research partnership on high-yield rubber tree genetics.

Looking ahead to the second quarter, the market enters the seasonal low-yield period with firming demand. New energy vehicle growth across Asia, an elevated oil floor, replanting investments and tightening supply all point to constructive pricing. Risks like trade disputes, weather extremes and geopolitical tensions remain, but March data shows an industry turning uncertainty into opportunity.

Comments (0)

ADD COMMENT