THE ANSWER: COLLECTIVE FARMING

- By Dr. Siju T

- October 19, 2020

The state of Kerala in southern India still accounts for over 70% of the tappable area and 75% of the national rubber production in India. Given the agro-climatic advantage, quality of human resources cultivating rubber and productivity of rubber, Kerala is expected to retain its prime position in Natural Rubber production in the near future. Though the area under rubber cultivation is increasing in the non- traditional regions, which has got cost advantages over the traditional region, it has inherent climatic disadvantages. A cost-benefit analysis by RRII revealed higher BCR (Benefit-Cost Ratio) for Kerala than in the non-traditional regions due to its higher productivity which offsets the higher cost in the state to some extent. So, maintaining the production sector in Kerala in good health is key to ensuring sufficient domestic production of rubber in the coming decades as envisaged in the National Rubber Policy (NRP) of India.

The NRP envisages sourcing 70% of India’s requirements of natural rubber through domestic production. This also gains importance as India has once again started thinking in the direction of self-sufficiency through its Atma Nirbhar Bharat initiative and the current domestic production of Natural Rubber accounts for just over 50% of the national requirement.

But the days of the smallholding sector of Kerala, which has scripted the success of rubber production in India from the 1980s onwards, seems to be over and running out of steam. The sector is in deep crisis as it is confronted with issues like uneconomic size of holdings, low price of natural rubber and scarcity of tappers. This paper analyses the persisting issue of scarcity of rubber tappers in the sector.

Widening demand-supply gap

The first census of rubber tappers conducted by Rubber Board in 2013 enumerated 77,207 tappers in the smallholdings sector in Kerala. The estimated tappers requirement to tap the existing tappable area of 4,56,000 ha in Kerala in the smallholdings sector under different systems of tapping is presented in Table 1.

The census revealed that 13.7 per cent (10,577) tappers were under S/2 d1, 81.2 per cent (62,692) were under S/2 d2, 4.7 per cent (3629) under S/2 d3 and 0.4% (309) under various other low frequency tapping (LFT) systems in the smallholdings sector. By assuming a stand of 400 trees per tapping block, these tappers could tap only 1,49,011 ha regularly. This shows there exists huge demand-supply gap of tappers in the sector, resulting in large number of holdings either left untapped or tapped irregularly.

Inherent structural bottlenecks

In the general agricultural sector of Kerala, helpers of masons in the rural construction sector are considered to be the most immediate group with whom agricultural labourers identify or that these segments of rural labour markets interact during short-term fluctuations in the supply and demand. Similarly, supply of tappers at a given point of time is determined to a great extent by the wage income of tappers and the wage rates prevailing in the sectors closely interacted by the tappers in the smallholdings sector. Lower wage income of tappers in relation to wage of agricultural labour and semi-skilled workers was reported as the main reason for aversion of younger generation to tapping job. Trends in the wage rate of tappers in the smallholdings sector of Kerala are presented in Table 2.

Based on the structural breaks observed in the wage rate of rubber tappers since 1980, the entire period was sub-divided into five. During the entire time period, except for the period 2014 to 17, the wage rate of tappers has been increasing in real terms. The highest growth rate in nominal and real wages was observed during 2005 to 2013. A plateau in the growth of nominal wage rate was observed after 2013 and hence the real wage rate showed a decline (Fig 1).

Though wage rate of tappers has been showing growth in nominal and real terms till 2013, the sector has been facing severe scarcity of tappers. This shows that increasing wage rate has not succeeded in attracting sufficient tappers into the sector. Hence, wage share, which is a measure of distribution of income between the capital and labour, was computed to know the distribution of income between the farmers and tappers in the sector. Trends in wage share of rubber tappers in nominal and real terms are presented in Table 3.

The wage share of tappers has increased in the last one decade both in nominal and real terms. Though wage rate of tappers has declined in real terms in the last few years under analysis (Fig 1), wage share has been increasing in the smallholdings sector. Increasing wage share in the sector indicated better distribution of income among the capital and labour.

Nevertheless, the wage rate of tappers, both in nominal and real terms, has been increasing (except for the past a few years) and the sector exhibited an increasing wage share in real terms, the sector failed to attract sufficient tappers, leading to severe scarcity. This warrants for deeper analysis to understand the issue. Hence, a comparison of estimated wage incomes of rubber tappers with agricultural labourers and helpers of masons in the construction sector was done and presented in Table 4.

The estimated annual wage income of rubber tappers in the smallholdings sector of Kerala was found to be 44 per cent and 59 per cent less than their counterparts in the general agriculture and construction sectors respectively. This makes the sector less attractive for the potential new entrants, which is ultimately reflected in tappers supply. Due to division and fragmentation of rubber holdings, the average size of holdings has come down and number of trees available for tapping was only 286 trees per tapping day under single grower dependence system and 75 per cent of tappers in the sector were engaged in the single grower dependence system.

In piece rate-based wage payment system, number of trees tapped per day and number of tapping days per year determines the annual wage income of tappers. Thus, in the present scenario, the smallholdings are incapable of giving more tapping task to the tappers to enhance their wage income. Hence, prevalence of single grower dependence, small size of holdings, lesser number of trees available for tapping per tapping day and the piece rate-based wage payment are the bottlenecks in enhancing wage income of tappers. But, in their effort to retain experienced tappers in the milieu of tappers scarcity, the farmers were forced to follow the labour intensive high frequency tapping systems with more tapping days, though it has implications on net farm income.

Even though the tapping wage rate and wage share has been increasing in real terms, the tappers are expected to demand a hike in the wage rate as the wage income earned by them is substantially lower than their counterparts in other rural employment sectors. In the present scenario, to make wage income of tappers on par with that of agricultural labourers and helpers in the construction sector, a hike of 79 per cent and 143 per cent respectively is required in tapping wage rate (Table 5).

But, an increase of this magnitude in the wage rate is not feasible as further hike in the wage rate would seriously affect sustainability of rubber cultivation as with the present cost of cultivation and price of rubber, the farm income is declining in real terms (Fig. 2) and wage share is increasing (Table 3).

Limited options

Since labour is becoming costlier and farm income has been declining in real terms due to uncertain prices, the options available with smallholdings are either to shift to other profitable crops or adopt cost saving technologies including mechanization as tapping accounts for more than 80 per cent of the labour requirement in mature rubber plantations. Generally, mechanisation is done as a labour saving process that occurs due to the increasing scarcity of labour most often reflected in a rising wage rate. But, since the scope for mechanisation in rubber tapping is limited and adoption of cost saving low frequency tapping (LFT) is constrained by the small size of holdings, farmers may either prefer to keep their plantations untapped or shift to other profitable crops. At present, as per Rubber Board data, around 30 per cent of the mature plantations are left untapped in the smallholdings. This will have serious implications on the rubber smallholdings sector as majority of the farmers are small and marginal with average size of holdings of less than 0.5 ha. A study conducted by the Centre for Development Studies, Thiruvananthapuram, found that the net operating income from an acre of rubber cultivation is only Rs. 16,732 in Kottayam and Rs. 19,681 in Thiruvananthapuram, which is not adequate to induce the rubber growers to continue with rubber cultivation. It was also observed that the recorded net income of those with holding size below 2 ha and depending only on rubber cultivation for their livelihood will be below the poverty line.

Thus, declining profitability is expected to dissuade small growers in Kerala from rubber cultivation and encourage them to explore alternatives. This will have far reaching consequences in the sector as the share of part time farmers are already high and a recent survey by the Economics Division, RRII revealed that for 69 per cent of farmers in Central Kerala, income from rubber accounted for less than 50 per cent of the total household income.

Collapse of the smallholder’s rubber sector in Kerala will have serious impact on natural rubber production in India as the state contributes nearly 78 per cent of total natural rubber produced in the country and the smallholdings sector accounts for nearly 90 per cent of area and production in Kerala.

Collectivism to circumvent the structural bottlenecks

Earlier studies have suggested methods like crop sharing and production incentives with annual compensatory allowances as alternatives to overcome the hurdles inflicted by the piece rate-based wage payment system and low tapping task in enhancing wage income of tappers to attract more tappers into the sector. But, large scale adoptions of these propositions were not reported in Kerala. Crop sharing is not sustainable in the long run as the return to capital is marginal and hence would deter large scale adoption by the small and marginal farmers. Production incentives to match the wage income of tappers to that of labourers in the general agricultural sector and helpers in the construction sector (Table 4 and 5) would render rubber cultivation uneconomical due to high cost of production in the smallholdings, which has long lost its economies of scale.

Prevalence of single grower dependence, small size of holdings and lesser number of trees available for tapping per tapping day being the critical bottlenecks in enhancing wage income of tappers and attract new tappers into the sector, any new system adopted should be capable of negotiating these bottlenecks efficiently to ensure tappers flow into the sector. Division and fragmentation of holdings aggravates these bottlenecks and render rubber cultivation uneconomical. Thus, as a measure to overcome these bottlenecks, collectivism/co-operative farming is suggested as an alternative. Collectivism would help to circumvent these structural bottlenecks of the smallholdings viz., small size of holdings, lesser number of trees available for tapping and prevalence of single grower dependence of tappers, as in collective farming the factors of production are pooled and the farm is managed as a single unit on co-operative basis. Hence under collectivism tapping task and wage income of tappers could be enhanced considerably. Willing farmers in the smallholdings sector can be bought under different farmer’s co-operatives and the farm can be managed as a single unit by professional managers under the supervision of the elected members.

Collective management of small rubber holdings under co-operative/collective farming would facilitate large scale adoption of cost saving technologies like LFT, as the holding size barrier for its adoption could be overcome by collectivism. Since the farm management decisions are implemented uniformly across the units managed under collectivism, it will have the advantage of economies of scale. Though LFT is recommended as a cost saving strategy in mature plantations to make rubber cultivation profitable, its large-scale adoption is constrained by the small size of holdings in the smallholdings sector.

The first census of rubber tappers by Rubber Board in 2013 recorded its adoption as below 5 per cent in Kerala. By following the LFT (S/2 d7) under collective farming, the tapping task and employment of tappers could be enhanced further (Table 6) and the wage income of tappers could be equated with their counterparts in the rural labour market. Table 6 reveals that with the present tapping wage rate itself, the wage income of tappers could be equated with the income earned by their counterparts in the rural economy under collectivism. In addition to higher wage income, the tappers attached to farmer’s co-operatives would have better access to welfare schemes extended for the tappers by the Rubber Board as the first tappers census observed poor percolation of the welfare schemes among the tappers, since the tappers in the smallholdings were unorganized.

The proposed collective farming is different from the activities performed by the Rubber Producers Societies (RPS). The present day RPSs are basically involved in technology dissemination, provide different services like subsidized input distribution, collective processing and marketing of NR. A few RPSs and Rubber Board promoted trading companies are organizing tappers under tappers banks to tap holdings which are either untapped or abandoned due to absentee farmers, non-availability of tappers and declining profitability due to price crash. Though tappers attached to the tappers bank under the present system get higher remuneration than their counterparts in the smallholdings (Table 7), this will not ameliorate tappers scarcity and encourage large scale adoption of LFT in the sector, as the bottlenecks discussed earlier remains.

In the proposed collective farming, farmer’s co-operatives are expected to play a major and direct role in rubber production by pooling the factors of production (plantations). The authority to make farm decisions would be vested with the co-operatives rather than individual farmers and the profit shall be shared among the members.

Conclusion

Though wage rate and wage share has been increasing in real terms in the small holdings sector, the wage income of tappers were substantially lower than the wage income of labourers in the general agricultural sector and helpers in the construction sector with whom tappers in the smallholdings relate in the rural labour market. Due to presence of structural bottlenecks as such as smaller size of holdings, lesser number of tress available for tapping, piece rate wage payment system and prevalence of single grower dependence, the sector was incapacitated to augment wage income of the tappers to equate it with that of labourers in other rural sectors. To attract more tappers into the sector by increasing the wage income of tappers by circumventing the structural bottlenecks, collective farming under farmer’s co-operatives following the principles of collectivism is proposed. Collective management of plantations will not only help the tappers to get regular employment, sufficient tapping task and remunerative wage income, it would also have the added advantage of bring down the cost of production of NR and increasing profitability of NR cultivation as it would also facilitate large scale adoption of labour and cost saving technologies for rubber production.

Rubber Board Extends Planting Aid Schemes At Current Rates For 2026-27

- By TT News

- May 08, 2026

The Rubber Board of India has confirmed the continuation of all existing central sector schemes for the 2026-27 fiscal year at unchanged rates. Financial aid for new planting will be restricted to estates utilising poly bag or root trainer plants sourced solely from Board-approved nurseries, with applicants required to submit the original purchase bill. This mandatory verification step aims to ensure quality and authenticity of planting materials used across the sector.

Support for rain guarding and spraying operations will be channelled exclusively through Rubber Producers’ Societies. These societies must include GST bills for all acquired materials when applying. The official timeline for submitting applications will be announced separately by the Board, giving producers adequate time to prepare documentation and coordinate with their respective societies before the deadline.

Rubber Board Calls For Marketing Graduates With Digital Skills For Temporary Engagement

- By TT News

- May 07, 2026

The Rubber Board of India has announced a temporary engagement for a young professional within its Market Promotion Division, located at the RRII campus in Puthuppally, Kottayam. The selected individual will assist with division activities and promote ‘mRube’, the electronic trading platform for natural rubber.

Candidates must hold an MBA in Marketing or Agri Business Management with computer knowledge, while skills in digital marketing, sales or market research and proficiency in English and Hindi are preferred. Applicants aged up to 30 years as of 1 May 2026, will be considered for the one-year role, which offers a consolidated monthly pay of INR 25,000.

Interested individuals should send their applications to the Deputy Director (Marketing) at the Central Laboratory Building, RRII, Rubber Board PO, Kottayam – 686009 by 19 May 2026. Shortlisted names will appear on the Rubber Board’s website with interview details, as no separate communication will be sent.

Bekaert Finalises Acquisition Of Bridgestone’s Tyre Reinforcement Plants In China And Thailand

- By TT News

- May 06, 2026

Bekaert has officially finalised its acquisition of Bridgestone’s tyre reinforcement operations in China and Thailand, after securing all necessary regulatory approvals and meeting standard closing conditions. The deal, now fully completed, marks a significant step in the Belgian company’s expansion strategy.

The transaction brings under Bekaert’s control two production facilities: Bridgestone (Shenyang) Steel Cord Co., Ltd. in China and Bridgestone Metalfa (Thailand) Co., Ltd. in Thailand. These plants specialise in manufacturing high-quality tyre cord products exclusively for Bridgestone tyres, and they will continue to supply Bridgestone under the new ownership, further deepening the longstanding partnership between the two firms.

Financially, the acquisition is expected to add roughly EUR 80 million to Bekaert’s annual consolidated sales. The EUR 60 million cash consideration for the deal was funded from the company’s available cash reserves.

Curd Vandekerckhove, CEO Rubber Reinforcement, said, “With the completion of this acquisition within our Rubber Reinforcement division, we are pleased to officially welcome the plant teams in China and Thailand to Bekaert. Our immediate focus is on a smooth transition and operational continuity while continuing to serve Bridgestone as a key strategic partner. The completion of the acquisition further strengthens the position of Bekaert in the tyre cord market, expands the global manufacturing footprint and deepens our longstanding partnership with Bridgestone. A long-term supply agreement ensures continued delivery of high-quality tyre reinforcement within a trusted supplier model.”

- Association of Natural Rubber Producing Countries

- ANRPC

- Natural Rubber

- Monthly NR Statistical Report

ANRPC Publishes Monthly NR Statistical Report For March 2026

- By TT News

- May 06, 2026

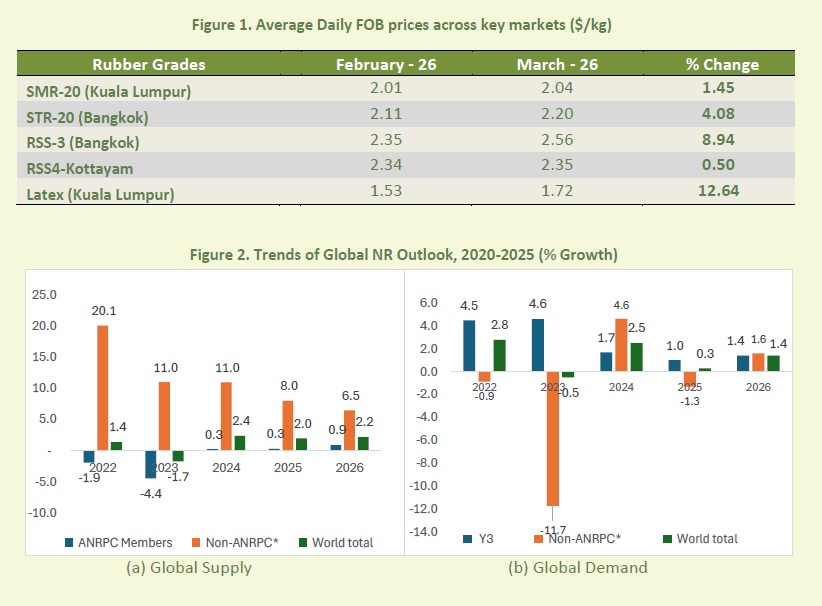

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly NR Statistical Report for March 2026, revealing a market that turned external pressures into clear price gains. While February had hinted at shifting dynamics, March provided proof of the industry’s core strength, with prices rising across all major grades and trading hubs despite an unusually challenging global environment. A 3.4 percent drop in monthly output and a dramatic 42.51 percent spike in Brent crude prices allowed natural rubber to advance rather than retreat.

Benchmark grades recorded widespread increases. In Kuala Lumpur, SMR-20 reached an average of USD 2.04 per kilogramme, while Bangkok saw STR-20 climb to USD 2.20 and RSS-3 jump to USD 2.56 per kilogramme. Kottayam’s RSS-4 averaged USD 2.35, and centrifuged latex in Kuala Lumpur rose sharply to USD 1.72 per kilogramme. Futures markets echoed the trend, with Shanghai’s May contract averaging CNY 16,662 per tonne and Singapore’s June contract closing at USD 1.95 per kilogramme.

The supply situation tightened considerably. Global March production is forecast at 786,000 tonnes, with Thailand’s output falling to 164,000 tonnes as southern growing regions endured temperatures of 42 to 43 degrees Celsius and rainfall up to 69 percent below normal levels. These punishing conditions sent a clear message that the market can absorb demand without chaotic price swings, a sign of a maturing commodity sector.

Demand told a similarly positive story. China’s natural rubber consumption surged from 446,000 tonnes in February to 610,000 tonnes in March, supported by a manufacturing PMI of 50.4, a 74.4 percent monthly rise in vehicle output, and a 130 percent annual leap in new energy vehicle exports. Chinese imports jumped 39.03 percent month-on-month to 629,800 tonnes, while Vietnam, Malaysia and Thailand boosted exports by 47.34 percent, 13.73 percent and 8.3 percent, respectively.

The oil market further strengthened natural rubber’s competitive edge. With Brent crude averaging over USD 101 per barrel and peaking at USD 126.69 on 31 March, synthetic rubber became significantly less cost-effective, giving tyre makers a strong incentive to favour natural rubber. Policy moves also bolstered confidence, including Malaysia’s replanting aid increase to RM 20,000 per hectare and a new Indonesian research partnership on high-yield rubber tree genetics.

Looking ahead to the second quarter, the market enters the seasonal low-yield period with firming demand. New energy vehicle growth across Asia, an elevated oil floor, replanting investments and tightening supply all point to constructive pricing. Risks like trade disputes, weather extremes and geopolitical tensions remain, but March data shows an industry turning uncertainty into opportunity.

Comments (0)

ADD COMMENT